Why the economics of coal helps us better understand the benefits of wind and solar energy

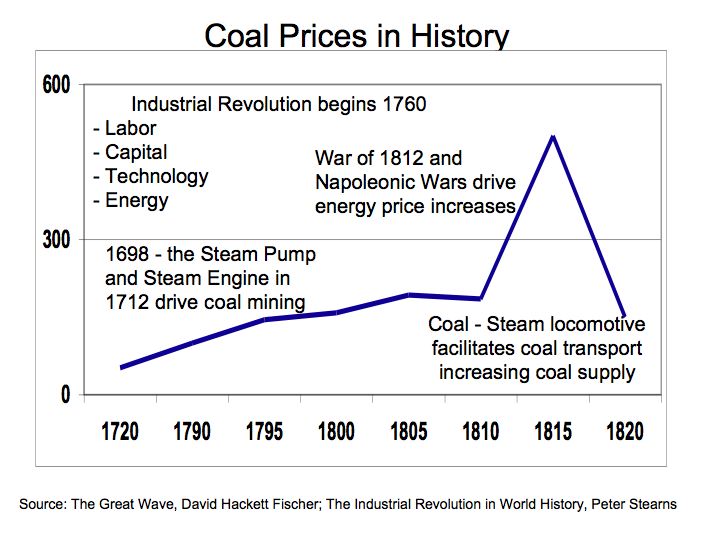

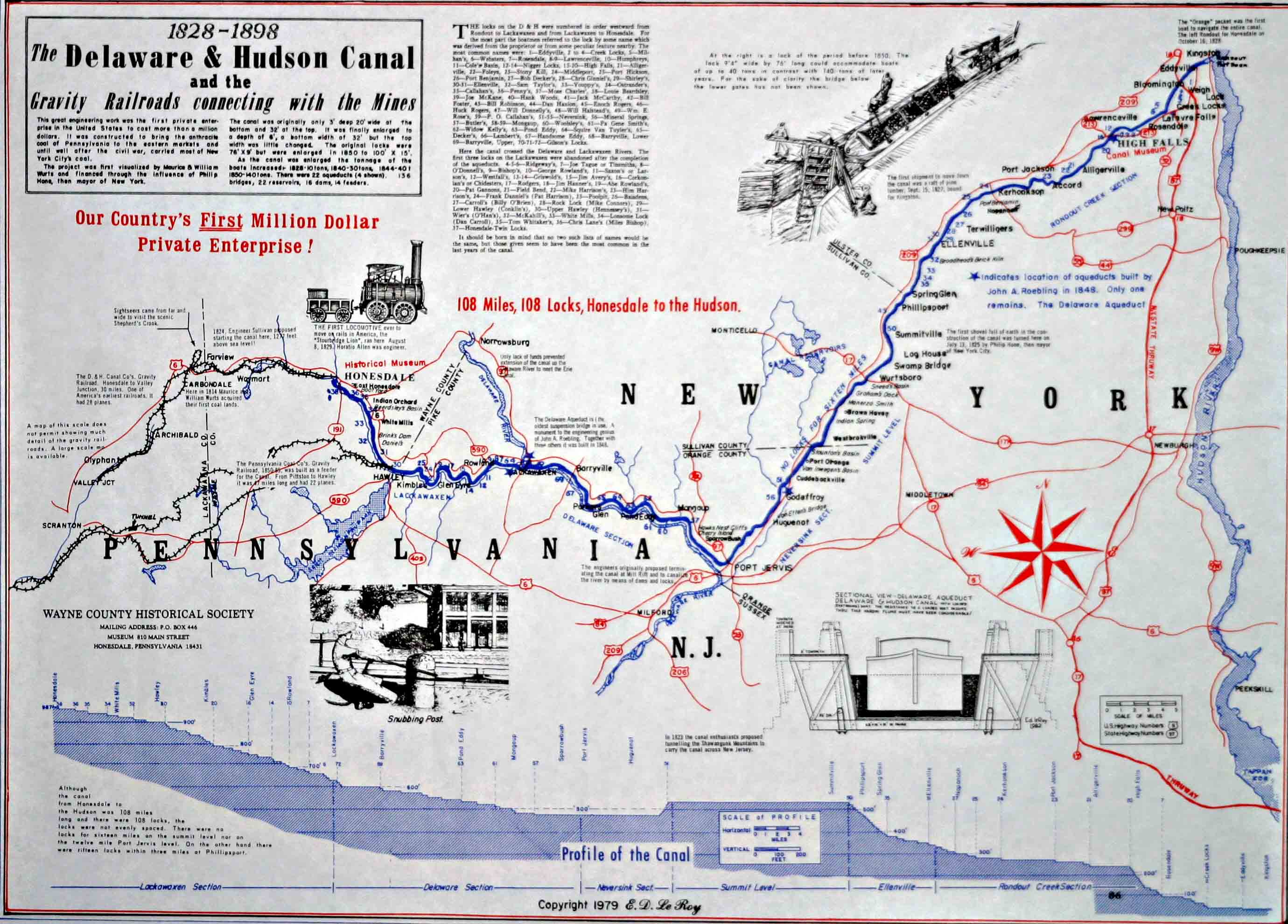

On August 8, 1829, the Stourbridge Lion made entry as the first American steam locomotive in Honesdale, PA initiating the American Railroad. The steam locomotive railroad was the first developed to transport Anthracite coal mined in nearby Carbondale, PA to a canal in Honesdale, linking to the Hudson River in New York.

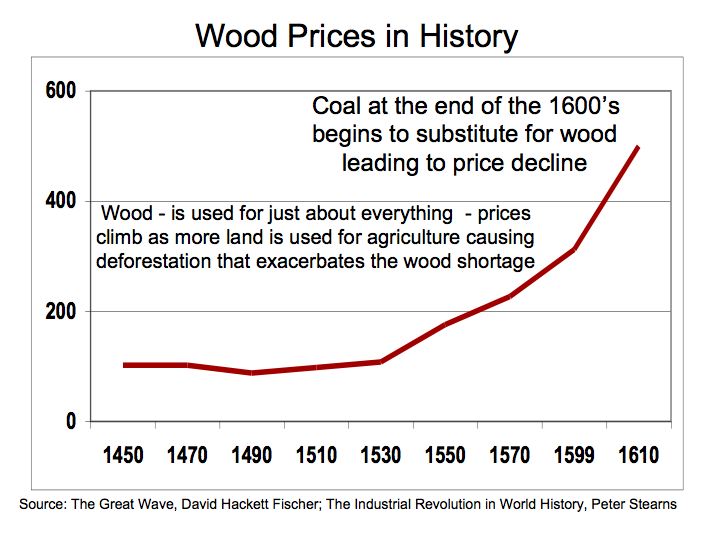

Coal as fuel energy has had an early use in American history with the 50 tons dug in 1748. Coal 1748 The history of coal dates backs to 2,000 BC and for oil it is even longer. Coal was cheaper and more efficient than wood. Coal was also more efficient to run most steam-powered engines, but was costly to transport and mine.

In terms of heating efficiency, coal offers almost double the energy, pound for pound, in comparison to wood. Energy Units and Conversions KEEP

Coal was difficult to mine and transport so engineers in America during the Industrial Revolution faced many challenges. Anthracite coal commanded a premium price because it emitted less smoke, was harder and contained more carbon giving it more fuel content than softer Bituminous or Lignite coals. There are several types of coal along a hard-to-soft classification. The makeup of coal changes according to compounds of lower hydrogen content and higher carbon – types of coal. Coal Ash Research Center University of North Dakota

The Anthracite coal deposits in Northeastern, PA are the largest deposit in the U.S. The gravity railroad linking Carbondale to Honesdale was an example of capital, knowledge, and technology meeting the growing need for energy.

Figure 1 Gravity Railroad

Coal was an important component for commerce and heating. With access to the large Anthracite coal deposits in Northeastern, PA, New York City gained an advantage over competing port cities like Boston and Philadelphia. It was the energy infrastructure of the railroad and canal transportation network that enabled New York to access coal. Essentially, coal provided the fuel for the Industrial Revolution and New York City’s ability to access coal to meet the needs of its growing population and commerce was critical to the city’s success. Honesdale, PA was named in honor of then mayor of New York. Wayne County Historical Society

To understand the economics of coal let’s start with a measurement of energy. One ton of coal is equal to 16.2-to-26 million BTUs (British thermal units) of energy. A BTU is the amount of heat necessary to raise one pound of water by one degree Fahrenheit.

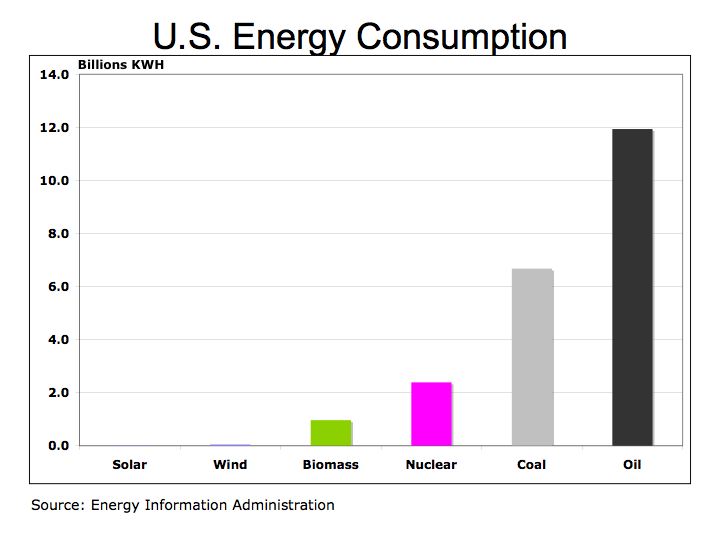

What is the economical value of a BTU? A common metric we should understand, particularly when we pay our utility bills is the kilowatt-hour – the amount of electricity consumed per hour. The KWH can be used to compare the efficiency and cost of wood, coal, oil, and gas. Also we can equate KWH to horsepower and have a common measure between energy usage and costs for our home and car.

Let’s convert fuel energy into a common equivalent. One-kilowatt hour (KWH) equals 3,413 BTUs. One ton of coal produces, on the average, 21.1 million BTUs, which equals 6,182 KWH of electric at a cost of about $36 per short ton (2,000 pounds). That means coal cost less than$0.01 per KWH. To put that into perspective, a barrel of oil at $77/barrel produces 1,700 KWH of electric equating to 60% higher efficiency pound for pound than coal. However, on a cost per KWH basis, oil cost about $0.05 per KWH. Coal’s lower cost per KWH is why it is still used today to generate electric.

Today, the Moosic Mountains who’s 1,940 foot pass became a formidable engineering challenge for transporting coal from Carbondale to Honesdale is adorned with wind mills from Florida Power & Light providing 64.5 megawatts of electric, enough to power 22,000 homes. Florida Power & Light

(FPL) is the largest generator of wind energy in the U.S. The irony is the mountain range with the largest deposits of Anthracite coal in the world and first used to provide electric to New York City, is now hosting windmills to generate electricity for homes and businesses.

Figure 2 Wind Energy

FPL is one of the growing list of utilities that are adopting alternative energy including wind energy programs in 15 states and offering rebates up to $20,000 for solar photovoltaic residential systems and up to $100,000 for commercial systems. The windmills atop Moosic Mountains produce electric replacing 3,800 tons of coal a year. A ton of coal produces 746 kg (1,644 lb.) carbon, so the windmills save our atmosphere from about 3,131 tons of CO2. The incremental increase in CO2 emissions should be added to the cost of coal because it has significantly higher carbon byproduct per KWH than oil or gas. Carbon content of fossil fuels

The coalmines are closed today along with the railroads and canals. Changes in the economic value of coal impacted numerous towns and villages across the region. Anthracite coal production in Pennsylvania reached its peak in 1917 when more than 100 million tons of coal was mined with the anthracite industry employment reaching its peak in 1914 with about 181,000 workers. Anthracite Coal

The value of coal diminished as demand shifted towards coke for iron and steel and oil became an energy substitute. The Carbondale region with its vast Anthracite coal deposits suffered as a result of falling demand for Anthracite coal. According the World Coal Institute, Anthracite coal has high carbon and energy content, but Bituminous coal accounts for majority of the world coal consumption because it is more abundant while coke is used in the iron and steel industry. World Coal Institute

The Northeastern, PA region experienced an economic shock as Anthracite coal lost its appeal. Demand shifted towards oil at the high end for transportation and the more abundant Bituminous coal at the low end. Anthracite represents only 8% of coal production today with Bituminous accounting for 76% and Lignite 16%. Those communities in Northeastern, PA that were more tightly linked to coal mining fell deeper into financial turmoil as the demand for Anthracite coal declined.

The Bottom Line: the economics of energy determines its use – coal still accounts for approximately half of our electric generation because it has a lower cost than other fuels. However, there are two factors to consider 1) the cost of carbon is not calculated into the full price of coal or other hydrocarbon fuels and 2) the cost of conventional fuel is calculated on a marginal basis while alternative fuel costs are calculated on a fixed cost basis. Meaning the cost of roads, trucks, and mining equipment is not factored into the price of each piece of coal, only the marginal cost of producing each ton of coal. For solar and wind energy systems, the cost to construct the system is factored into the total cost while the marginal cost of producing electric is virtually free. We need a framework to better measure the economics of alternative energy.

Despite the carbon issues surrounding coal, (coal has higher carbon-to-hydrogen ratio in comparison to oil or gas) coal is more abundant and therefore is cheaper than oil. Utilities could migrate to natural gas to reduce carbon emissions, but with a cost of $0.03 per KWH, there is no economic incentive. Alternative energies such as wind and solar could provide a longer economic benefit to users, our environment, and the economy.

Our next step is to develop a framework to measure the fixed and marginal costs of alternative energy.