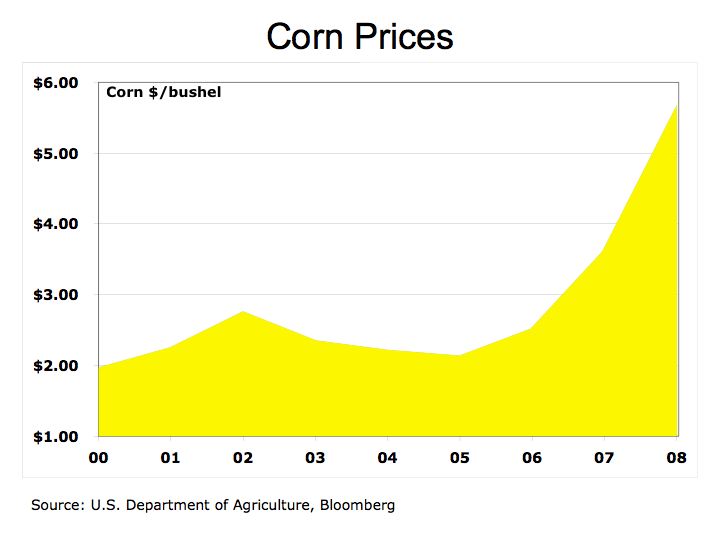

Solar energy is gaining considerable attention from Wall Street and countries looking to achieve energy independence. Solar energy represents one of the most significant energy solutions to help eradicate our addiction to oil. Despite the tremendous success offered with solar photovoltaic (PV), more research is required to sustain further deployment and achieve energy independence. Some semiconductor materials used to develop photovoltaic devices are scarce and may limit PV from achieving mass penetration. Let’s review the current solar PV market to better understand the dynamics of this market.

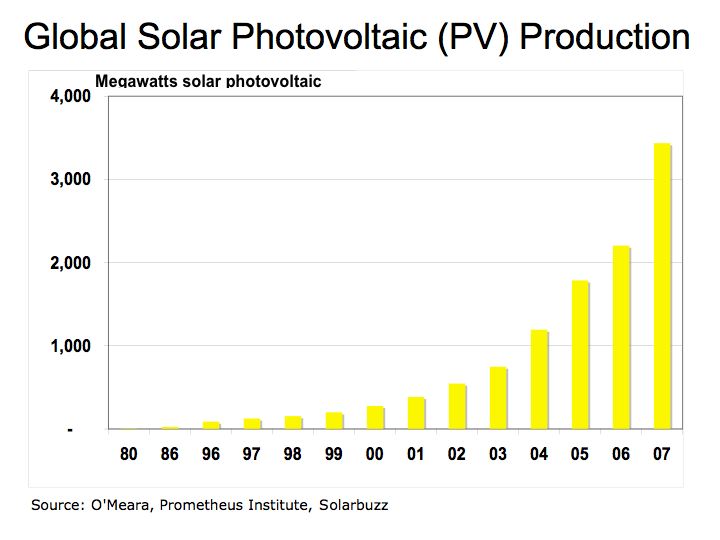

Figure 1 PV Production by Year

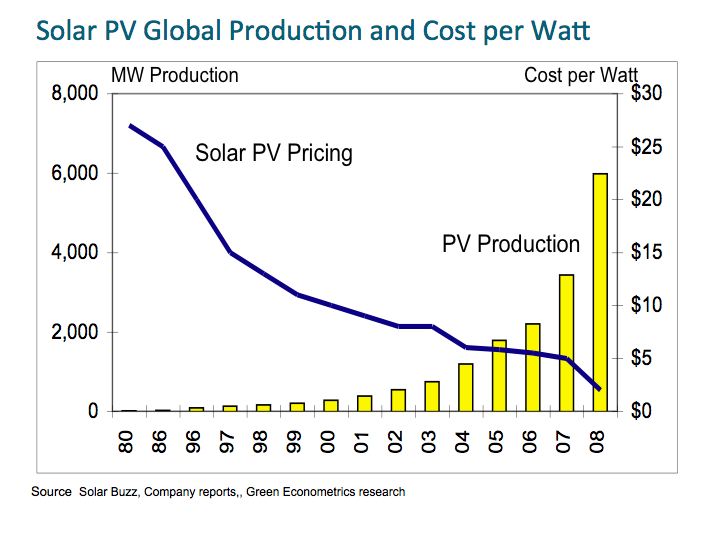

Figure 1 demonstrates the rapid market growth of solar PV and Solarbuzz is astute to point out some critical data points: cumulative PV deployment is still less than 1% of global electric usage, PV industry faces capacity constraints, and Germany and Spain account for 47% and 23% of total PV deployment in 2007. With the significant growth in both the production and deployment of solar PV devices, the stock price of some of the leading PV suppliers have appreciated dramatically even despite a recent pull back in the beginning of the year.

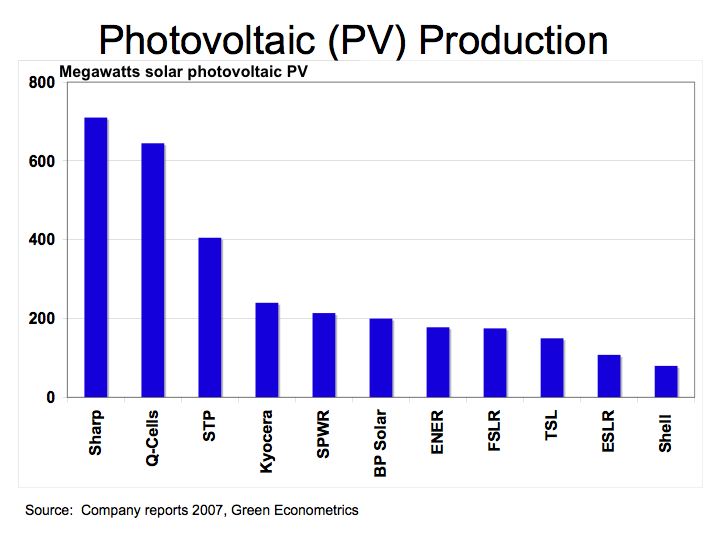

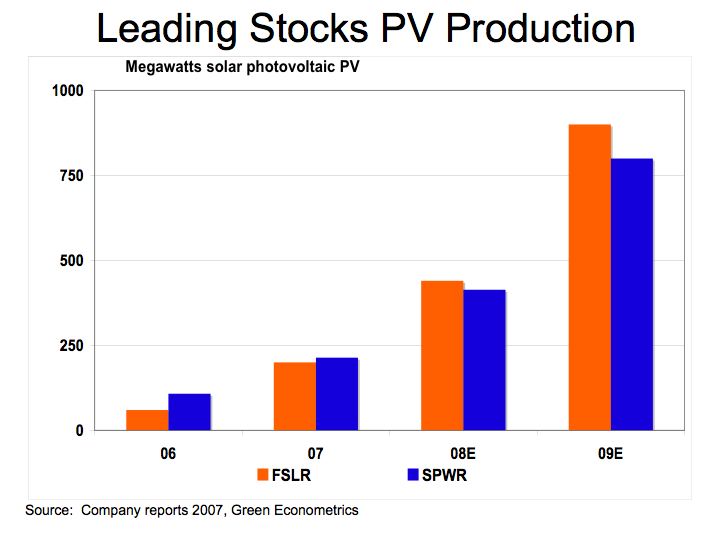

Figure 2 PV Production of Leading Suppliers

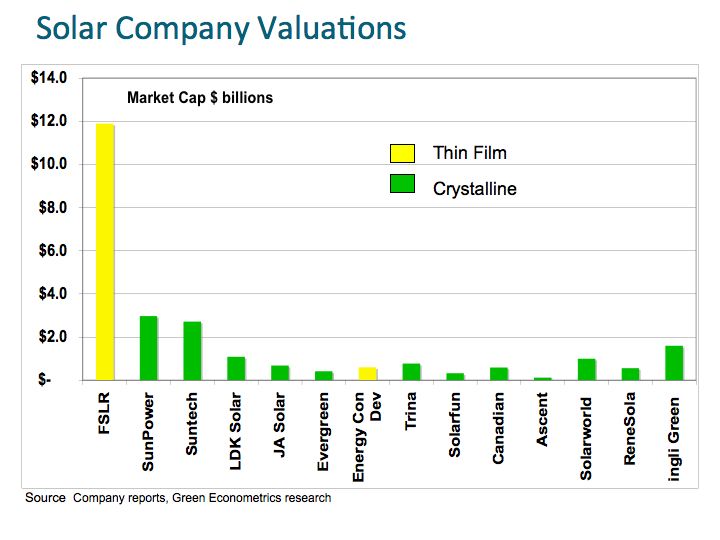

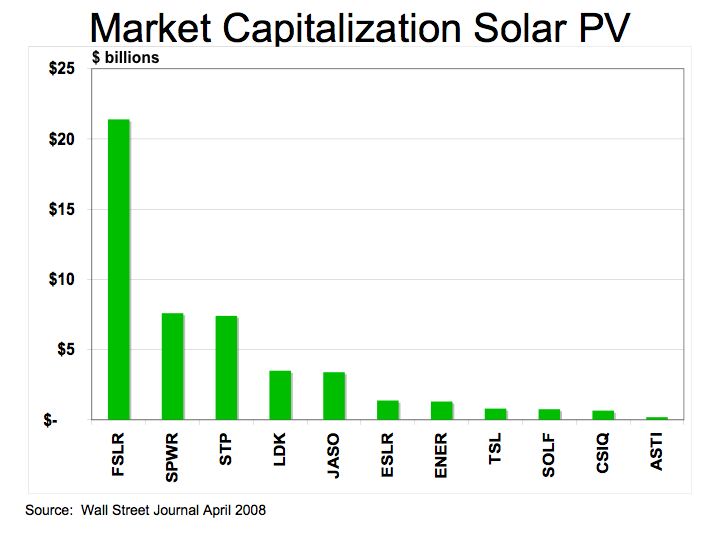

Despite the turbulence on Wall Street in 2008 with the NASDAQ down 14% year-to-date, and Dow Jones Industrial Average down 7.3% YTD, investor appetite for clean technology stocks remains robust. First Solar (FSLR), a leading supplier of thin film solar PV remains in positive territory and is up nearly ten-fold from its IPO in November 2006. Thin film PV offers a cost advantage over traditional crystalline PV cells. PV devices employ various elements with different band gap properties to achieve improving solar efficiencies. (See our post on semiconductor band gaps: What’s Pushing Solar Energy Efficiency?, October 1st, 2007)

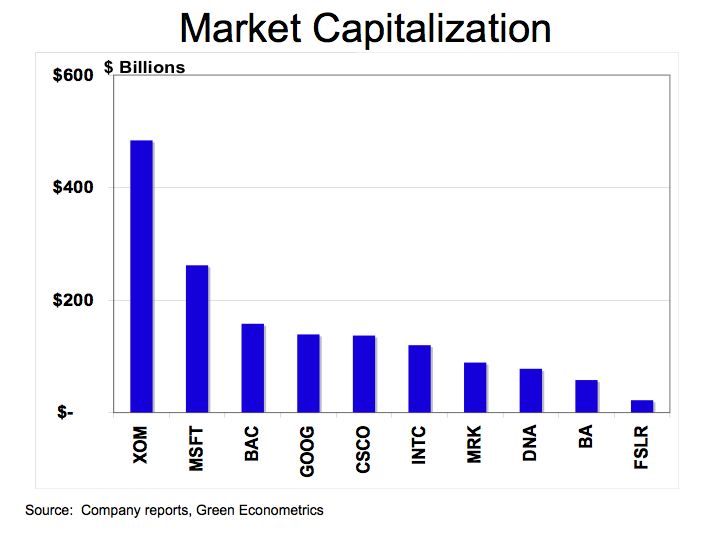

Figure 3 Market Capitalization Solar PV Suppliers

There are several elements used in thin film PV production. Among the elements used include cadmium and tellurium (CdTe), copper, indium, and selenium, (CuInSe), and copper, indium, gallium, and selenium (CIGS). These various elements are used to improve operating efficiencies and lower production costs of PV devices. In general, crystalline PV devices have higher solar efficiencies, but cost more due to their material thickness of 200-to-300 microns. Whereas, thin film PV are usually about 3 microns deep offering significantly lower production costs. However, SunPower (SPWR) the leading polycrystalline silicon PV supplier offers the highest solar efficiency a rating of 22.7% that started shipping in 2007.

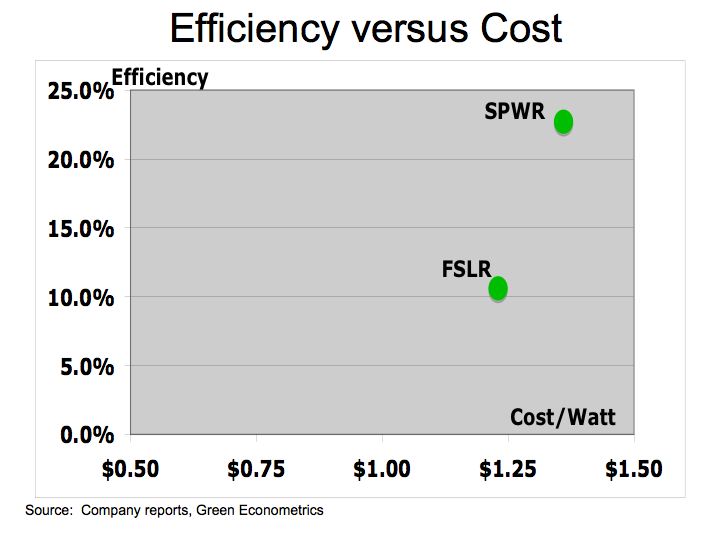

Figure 4 FSLR and SPWR Solar PV Production

FSLR and SPWR are the two leading PV players as measured by Wall Street in terms of market valuation. The cost-efficiency tradeoff between these two PV suppliers offers an interesting framework to evaluate the solar PV market.

Figure 5 PV Cost-Efficiency

The stock market appears to be betting on FSLR given its market capitalization of $22 billion and trading at 43 times 2007 revenues of $504 million. FSLR employs CdTe in its solar modules. In several postings on Seeking Alpha starting back in November 2007, Anthony and Garcia de Alba have provided valuable insight into material constraints in the production of PV devices.

Tellurium is a rare metalloid element that is used in producing semiconductor materials because it does not conduct electricity. Tellurium is recovered as a by-product in refining and processing of gold and copper as well as other ores. Tellurium was primarily used to create metal alloys that enable easier machining of end products.

Because of its unique properties, Tellurium and cadmium (CdTe) have been used in thin film PV production since the 1980’s. According to a comprehensive study by Fthenakis and earlier work by Moskowitz “The Life Cycle Impact Analysis of Cadmium in CdTe PV Production”, CdTe is deposited on a thin film substrate using electrodeposition, chemical surface deposition, and vapor transport deposition. FSLR reports in their 10K that they employ a proprietary vapor transport deposition process for CdTe PV production.

A thin film of CdTe is deposited on a substrate at a thickness of 3 microns. According to the Fthenakis and Moskowitz, back in the 1980’s, a 10 megawatt (MW) PV facility employing vapor transport deposition of CdTe uses 3,720 kilograms (kg) of CdTe to achieve a10% efficiency at 3 microns. A one-one bond of CdTe with an atomic weight of Cd at 112.41 and Te at 127.60 suggests Te comprises 53% of the weigh of CdTe. With 3,720 kg of CdTe used at 10MW, the amount of Tellurium used is estimated at 1,978 kg or 197.8 kg/MW.

The electrodeposition CdTe process using a mixture of cadmium sulfate and tellurium dioxide used 880 kg of tellurium dioxide, which amounts to approximately 696.8 kg of Te for 10 MW PV productions. The electrodeposition CdTe process would equate to about 69.7 kg of Te per MW. For a 100 MW PV production approximately 7 tons of Te are consumed.

One would assume the PV production process would improve significantly from the 1980’s and the amount of Te consume would decline with improving efficiencies. This would suggest that FLSR at 200 MW PV capacity in 2007 would consume somewhere between 14 and 38 metric tons of tellurium. This figure is significantly higher than the estimates derived from the FSLR tellurium posts on Seeking Alpha that are closer to10 tons per 100 MW (100 kg/MW).

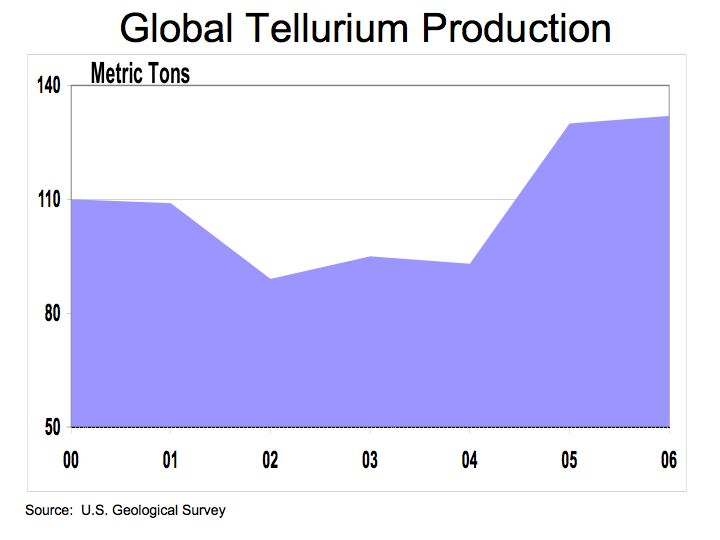

Figure 6 Te Production

Let’s proceed with the conservative figure of 100 kg/MW (10 tons at 100 MW) to assess the tellurium constraints. Tellurium production is a by-product of gold, copper and other ores. We have found Te production estimates ranging from 132 metric tons (MT) to 300 MT per annum. In a National Renewable Energy Laboratory (NREL) report Assessment of Critical Thin Film Resources in 1999 estimated Te production between 200 and 300 metric tons per year in 1997 and indicated under utilization of capacity for the production of tellurium.

Let’s compare our conservative estimate of 100kg/MW Te usage for FSLR to the optimistic production forecast of 300 MT to evaluate capacity constraints for FSLR. With 300 MT (300,000 kg) global Te production and FSLR using 80% of the Te production, capacity of PV tops out at 2,400 MW (2.4 GW).

The U.S. electric energy usage in 2006 was 4,059.91 billion kilowatt hours (KWH) which translates into 463,460 MW (divide 4060 by 365 days x 24 hours). So without significant investment into research and development for PV FSLR could be constrained at 2,400 MW representing only 0.5% of the U.S. electric usage in 2004. Further more, if FSLR were to be constrained at 2.4 GW annual production, revenues ($2.60 per watt Q4/07) would peak at approximately $6.24 billion, a price-to-sales multiple of 3.4x with its market capitalization of $22 billion.

However, in comparison to leading companies in energy, pharmaceuticals, technology and finance, FSLR’s market capitalization is relatively small. Perhaps with improving production processes, FSLR could reduce the amount of Te per panel and improving mining and metal refinement process could increase Te production to expand the market for CdTe thin film PV devices.

Figure 7 Market Capitalization of Leading Companies

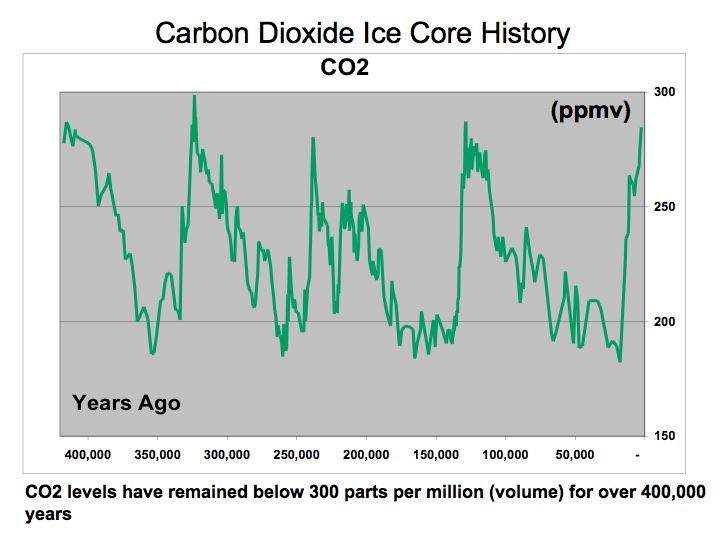

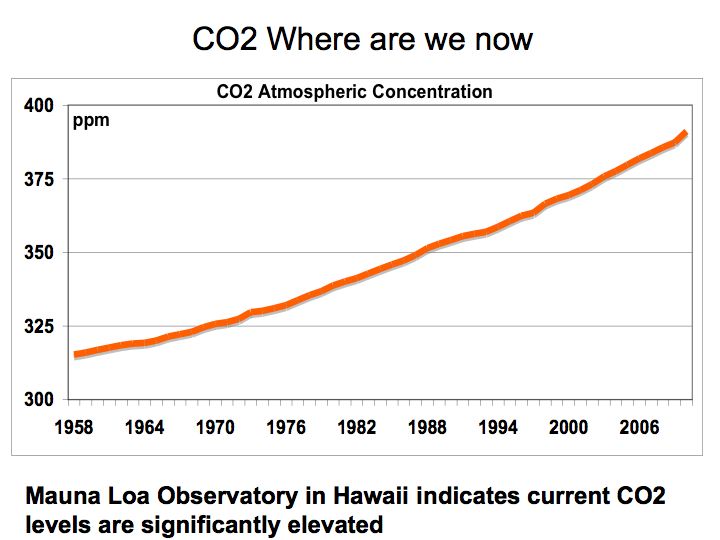

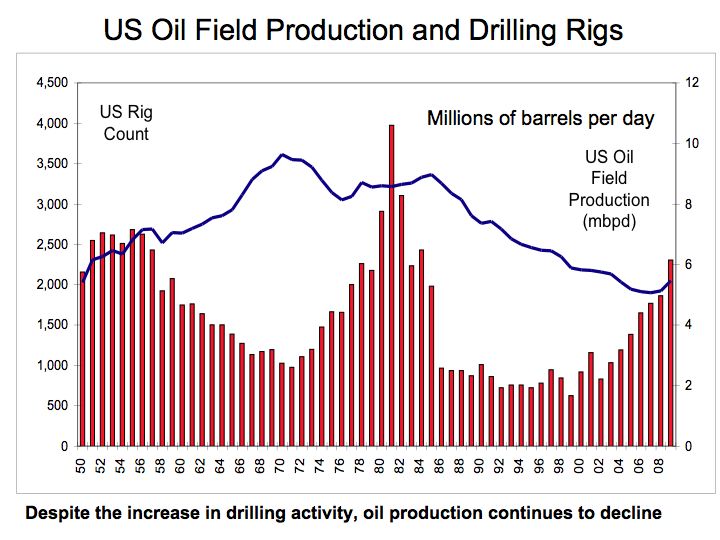

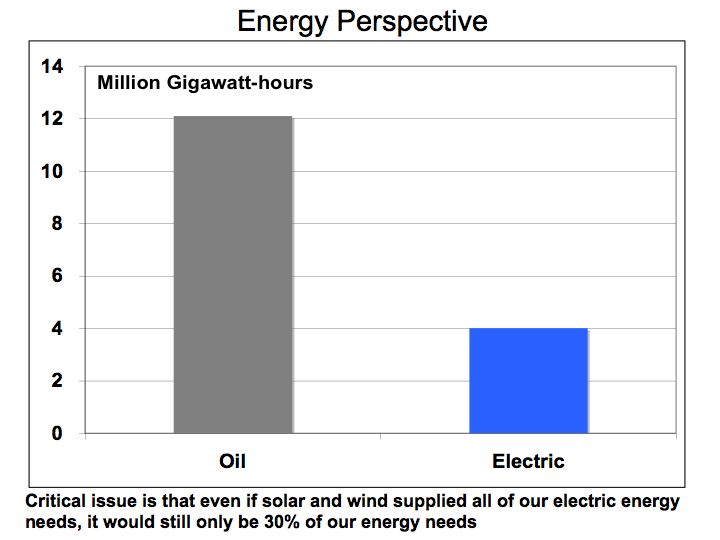

The bottom line is that more research and investment into alternative energies is required to ameliorate the world from being held hostage to oil and hydrocarbon fuels that are directly linked to rising CO2 levels and climate change.