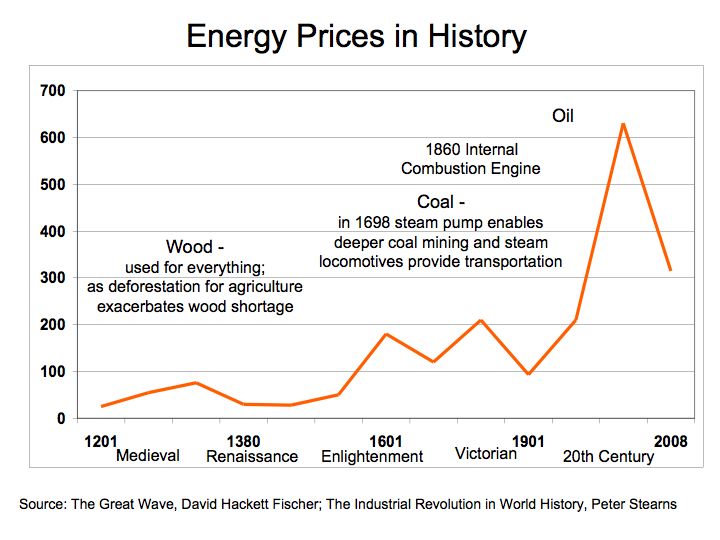

The development of an energy efficiency strategy incorporates analysis of energy expenditures and energy consumption. The energy strategy must incorporate dynamics between costs, budgets and the consumption of energy including the monitoring of kilowatt-hours (KWH) of electricity and liquid hydrocarbon fuels consumed. By analyzing both the financial and the energy consumption components we are better positioned to frame the scope of the energy efficiency projects.

We start with a comprehensive energy audit analyzing energy consumption and expenditures. After determining which activities offer the fastest, cheapest, and greatest economic impact we are then able to define the scope of energy efficiency projects. The next step in the energy strategy process is to assess, rank and specify energy saving opportunities. At this phase, we have a broad understanding of the scope of energy efficiency projects within the appropriate budgetary considerations.

Conduct Energy Audit and Analyze Energy Spending

Upon analysis of the energy expenditures and the appropriate budgetary considerations, we commence with an energy audit to examine the dimensions of energy consumption. The energy audit establishes an energy efficiency baseline for buildings and vehicles. In the energy audit, energy consumption is measured by source and activity using monitors attached to branch circuits, gas pipes, and fuel lines. In this manner, energy consumption is evaluated from a financial and physical perspective and baseline usage patterns are established for electricity and other fuels.

During the energy audit, an analysis of energy intensity is measured. For buildings, energy consumption is measured in kilowatt-hours per square-foot to identify which activities consume the most energy. The energy intensity measurements are then ranked by consumption activity and compared to actual energy expenditures.

The purpose of the energy audit is to establish a baseline of energy consumption and the energy intensity associated with each building, department, vehicles, and/or activity usage category. By constructing an effective energy efficiency strategy that identifies and measures energy demand by activity, a better understanding of economic- and financial-impact is established. The critical component to the energy audit is measurement and verification were wireless Internet-based energy monitoring provide data before and after energy efficiency projects commence. The energy audit and energy monitoring systems together with financial analysis of energy consumption serve as the framework to rank and assess energy efficiency projects.

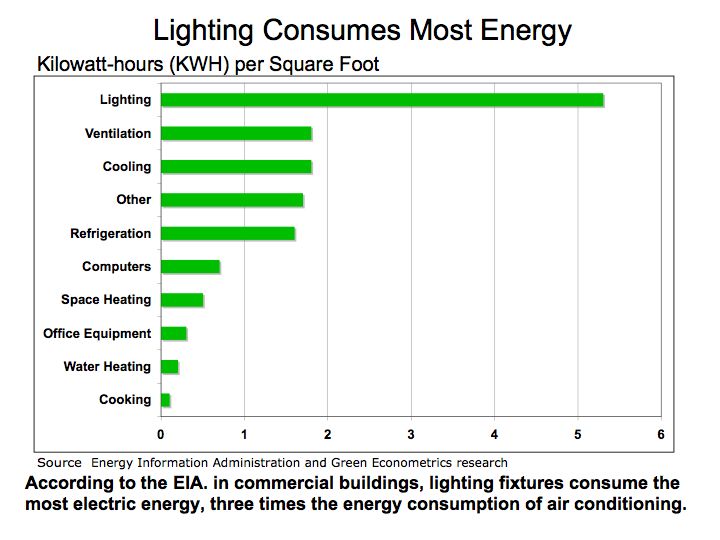

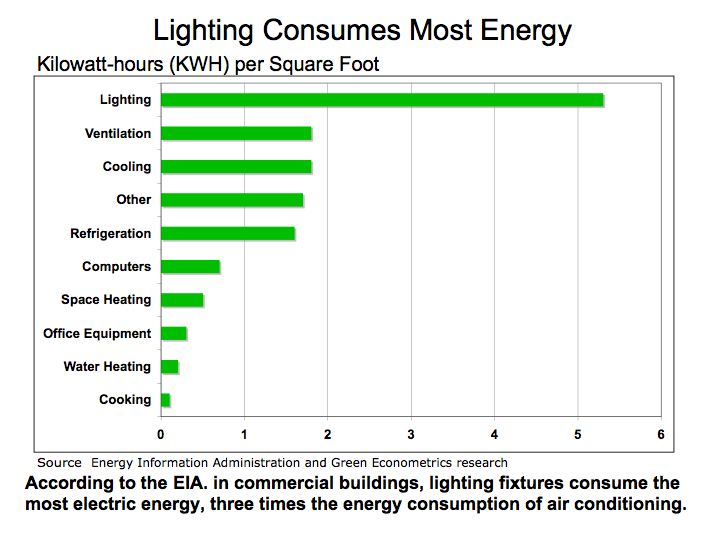

Heuristically, energy consumption in buildings is tied to lighting; and heating, cooling, and ventilation systems see Energy Intensity . The following chart, Figure 1 serves to illustrate which activities contribute most to energy consumption in buildings.

Figure 1 Kilowatt-hours (KWH) per Square Foot

According to information provided by the DOE, lighting, cooling and ventilation alone account for nearly two-thirds of all energy consumption in a building. For perspective, electric energy demand is increasing at an annualized rate of 1.6%. According to the Energy Information Administration (EIA), demand for electricity grew 21% between 1995 and 2006.

The energy consumption audit provides a means to assess which activities should be further analyzed for energy efficiency projects. The baseline energy usage measured in KWH per square foot serves as the framework to evaluate that locations and activities could benefit from lighting retrofits, equipment upgrades, structural improvements, and energy monitoring systems.

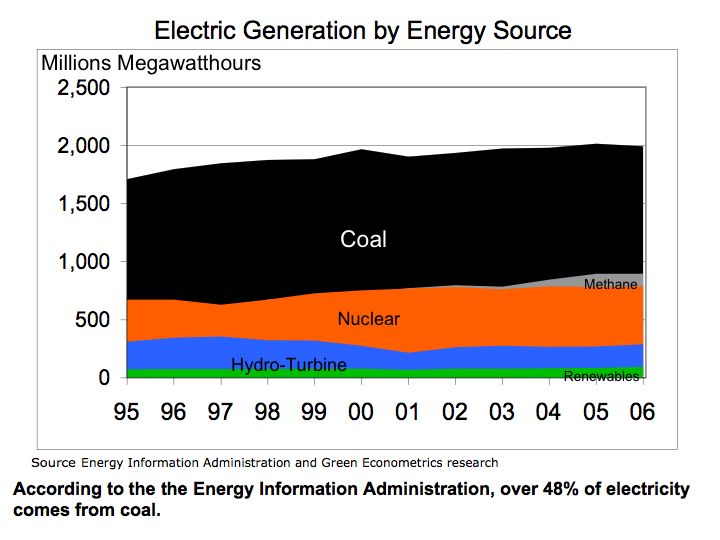

As a consequence of increasing energy consumption in buildings, electric generation relies extensively on hydrocarbon fuels that carry adverse environmental effects. Figure 2 illustrates the proportion of coal and other hydrocarbon fuels that are used to generate electricity in comparison to renewable energy sources. Coal still accounts for nearly half of all electric generation while contributing the most in terms of harmful emissions such as carbon dioxide, nitrous oxide, and sulfur dioxide.

FIGURE 2: Electric Generation Method

As part of the energy audit process for buildings, an energy consumption analysis of lighting and HVAC systems is evaluated along with the building’s insulation R-Value (resistance to heat flow where the higher the R-value, the greater the insulating effectiveness). In addition to lighting and HVAC systems, specialized equipment may also account for large energy demand. During our energy audit, we plan to identify and measure energy usage of special equipment in order to construct energy efficiency initiatives with clearly defined and measurable energy reduction targets.

Energy efficiency for transportation vehicles is one of the most significant factors to manage. The fact that there are no real substitutes for oil in the transportation industry illustrates two important points: 1) structural changes to driving patterns are required to see appreciable changes to oil consumption and 2) government authorities are vulnerable, with no readily available substitutes for oil, supply disruption could negatively impact transportation systems. Therefore, we emphasize fuel management systems for fleets and vehicles that monitor fuel consumption and efficiencies. DOE studies have indicated that changing driving habits could improve fuel efficiency by up to 30%.

Vehicle mounted devices that integrated fuel consumption feedback as the vehicle is driven promotes higher fuel efficiency. These off the shelf products are cost-effective, offering payback in months that dramatically improves fuel efficiencies. Aside from routine tune-ups, limiting weight, and checking tire pressure, augmenting driving patterns through gauges that provide feedback on fuel efficiency make the difference in saving energy.

In most situations, fuel management systems can be installed without significant mechanical aptitude. The ScanGaugeII from Linear-Logic is useable on most vehicles manufactured after 1996 including Gas, Diesel, Propane and Hybrid Vehicles and are designed to be installed by the consumer with plug-and-play instructions.

Identify and Measure Energy Demand by Activity

From the Energy Audit, the energy intensity of targeted buildings and fuel efficiencies of official vehicles are established. In buildings, it’s the lighting and heating, ventilation, and cooling that comprise the bulk of energy consumption.

Heating, ventilation, and cooling represent a significant portion of energy consumption in buildings and are a priority target for energy analysis. The Seasonal Energy Efficiency Ratio (SEER) is employed as an assessment of the equipment and analyzed in conjunction with building insulation. The efficiency of air conditioners is often rated in SEER ratio, which is defined by the Air Conditioning, Heating, and Refrigeration Institute and provides a standard unit measure of performance. The higher the SEER rating of a cooling system the more energy efficient the system is. The SEER rating is the amount of BTU (British Thermal Units) of cooling output divided by the total electric energy input in watt-hours.

For heating systems in a building, Annual Fuel Utilization Efficiency (AFUE) is used to measure and compare the performance of different systems. DOE studies have indicated that even with known AFUE efficiency ratings, heat losses defined as idle losses contribute to degradation in heating system efficiency,

To analyze energy consumption of heating and air conditioning systems (HVAC), we evaluate the building’s R-Value in comparison to the energy efficiency of the current heating and air conditioning systems. The energy demand evaluation includes a cost-benefit analysis comparing options in either HVAC system upgrade and/or improvements to the building’s insulation R-Value. By comparing the buildings R-Value in conjunction with HVAC efficiency performance, projects offering the greatest cost effectiveness are identified. The building’s R-Values can be measured using FLIR Systems infrared camera and software system. In this manner, the replacement cost of an HVAC system and costs to improve the building’s R-Value are analyzed to measure economic benefits. This information will allow the building owner to make an informed decision on whether any energy efficiency investment into HVAC upgrade or improvement to R-Value demonstrate economic benefit, i.e. positive financial return.

Consideration for heating and cooling systems upgrades are assessed by equipment SEER and AFUE ratings, installation costs, and efficiency payback. After equipment assessment is complete, proposals will be provided along with estimates for upgrade costs and payback analysis.

Benchmark and Analyze Energy Intensity

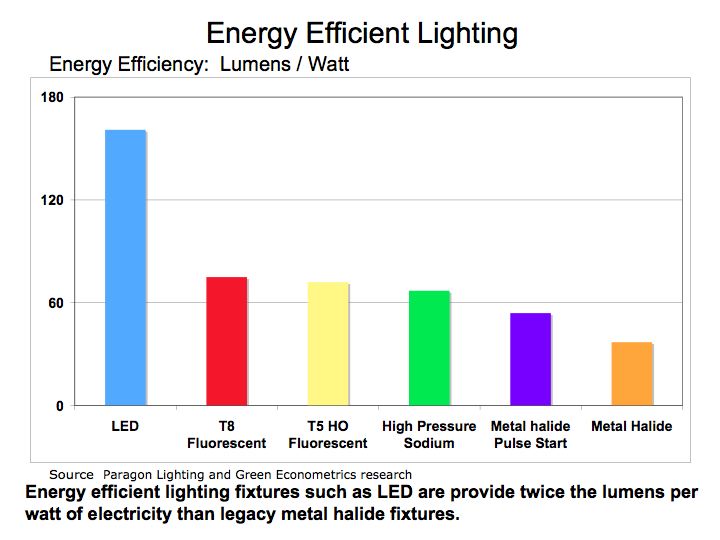

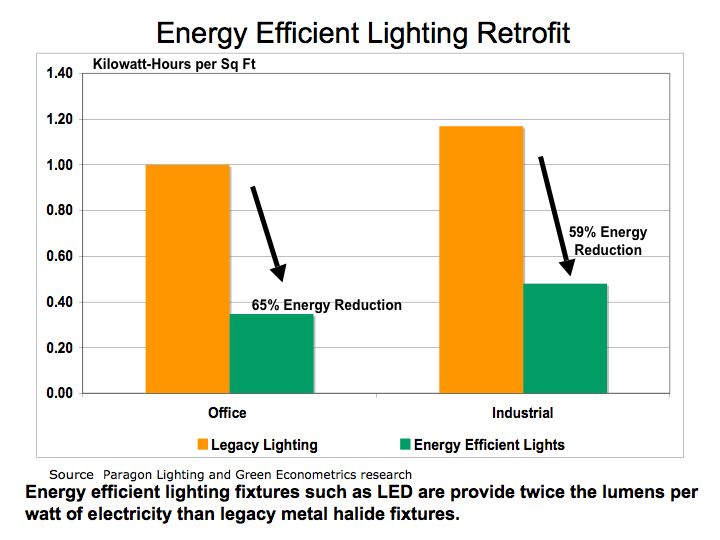

After conducting the energy audit, and compiling data on energy usage by activity category, we benchmark and analyze energy projects offering the greatest opportunities. As illustrated in Figure 3, energy efficiency for lighting systems can be substantially improved by retrofitting legacy light fixtures with higher efficiency fixtures and bulbs.

The energy audit and analysis provide the framework to evaluate energy efficiency projects. By analyzing energy consumption and the economic benefits associated with the energy savings projects, the most efficient and economically beneficial initiatives are identified and ranked.

FIGURE 3: Energy Savings in KWH per Square Foot Figure 1 Kilowatt-hours (KWH) per Square Foot

Establish Measurable Goals and Objectives

To establish relevant goals and objectives we are evaluating projects that are adhering to the SMART goal approach: specific, measurable, attainable, realistic and timely. Energy efficiency gains are most pronounced with lighting retrofits and energy monitoring in buildings in buildings and energy monitoring in vehicles.

After conducting an energy audit, analyzing energy consumption activities and the economics of energy efficiency projects, realistic and achievable energy savings goals are defined. Key performance metrics for energy savings are defined for buildings and vehicles. Key performance indicators are established for each project. For example, KWHs saved are defined for lighting retrofit projects, efficiency improvements for HVAC system upgrades, R-Value improvements for building insulation, and MPG gains for vehicles.

For each energy savings project, timelines are established with clearly defined milestones. Energy projects are presented with costs; expected energy savings measured in energy and dollar units, cost benefit analysis, and timelines.

Architect the Deployment of Energy Monitoring Systems

One of the first energy initiatives to consider in any energy savings project is the installation of an energy monitoring system for vehicles and buildings. Energy monitoring systems demonstrate the fastest and most economical pathways to achieving energy savings.

Energy monitoring systems for motor vehicles also demonstrate positive economic returns and real energy savings. The $180 energy-monitoring device with 10% fuel efficiency gain achieves breakeven at 14,500 miles with gasoline costing $2.50 a gallon.

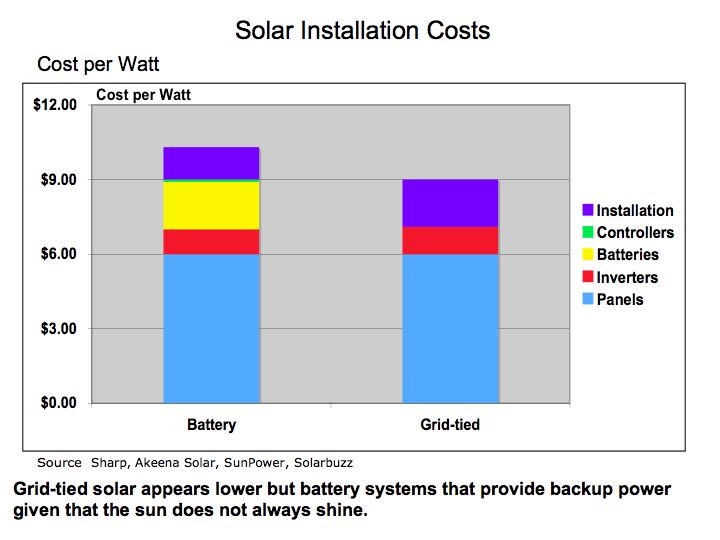

Evaluate Feasibility of Renewable Energy Projects

Renewable energy projects such as solar and wind energy systems are often costly with long payback periods. Without tax incentives and grants, renewable energy projects are unable to demonstrate positive financial returns. However, utility rates for electric are expected to increase, improving the case for renewable energy projects. To improve the viability of alternative energy projects, energy efficiency projects such as lighting retrofit serve to lower energy consumption and therefore enhance the feasibility of solar and wind energy projects.